The resolution authorities work with institutions during the normal course of their activities, to plan the actions that would be needed in the event that the institution fails or is likely to fail in the near future.

These actions are planned by the Single Resolution Board (SRB) and the Banco de España through the development of “resolution plans”.

The resolution plan is drawn up by the competent resolution authority in its capacity as the preventive resolution authority and contains three key elements: 1) the tools that would be used to restructure the institution, 2) a resolvability assessment of the institution, to identify any impediment to applying these tools, and 3) the MREL (only in the case of institutions with a resolution strategy).

Conditions for resolution

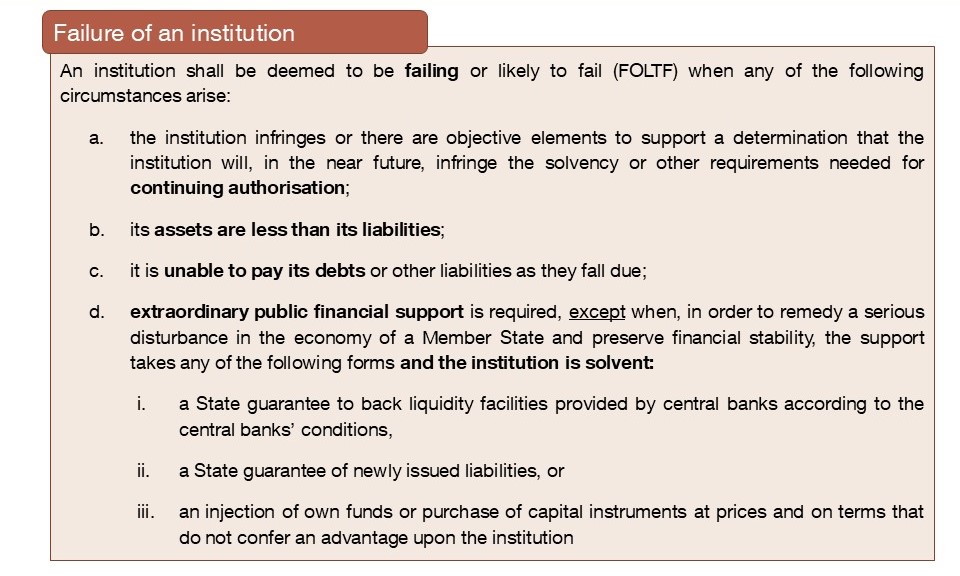

When an institution is identified as failing or likely to fail in the near future, first the feasibility of winding up the institution under normal insolvency proceedings is assessed, in which case the covered deposits would be reimbursed by the Deposit Guarantee Scheme. If deemed to be in the public interest, resolution tools will be applied to protect the essential services provided by the institution to the public and firms and to preserve financial stability.

The decision on when a significant institution is failing or likely to fail in the near future is determined by the European Central Bank (ECB). The SRB may also make this assessment, but it may do so only after informing the ECB of its intention and only if the ECB, within three calendar days of receipt of that information, does not make such an assessment. In the case of less significant institutions, the competent supervisory authority determines whether the institution is failing or likely to fail. Subsequently, the Spanish executive resolution authority (FROB) analyses whether the other circumstances for initiating the resolution procedure exist.

The SRB (or the FROB, in the case of institutions within its remit) is responsible for determining whether resolution is necessary in the public interest. If this condition is not met, the institution would be wound up under normal insolvency proceedings.