Background and regulation

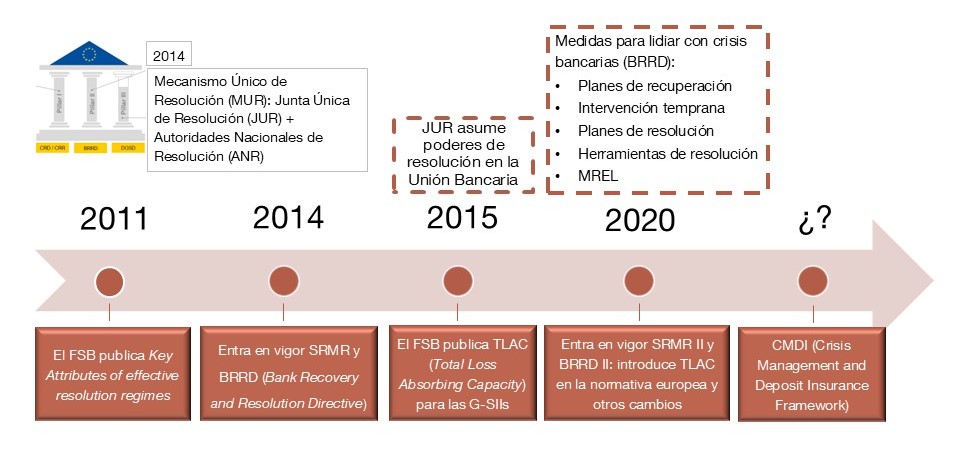

The 2008 financial crisis exposed the inadequacies of the tools available to the financial authorities for handling bank failures in an orderly fashion. The crisis led the G20 to prioritise developing and implementing specific powers for the public authorities for managing bank failures (resolution), and in October 2011 it endorsed the Financial Stability Board’s (FSB) “Key Attributes of Effective Resolution Regimes for Financial Institutions”.

This document is an international benchmark used by all FSB members when setting up their legal resolution framework. In the European Union, it was implemented through the Bank Recovery and Resolution Directive (BRRD), which provides the resolution authorities with the powers and tools to intervene in those institutions that have been identified as failing or likely to fail in the near future. In addition, the Single Resolution Mechanism and the Single Resolution Board were created. In Spain, the BRRD was transposed into national legislation through Law 11/2015 of 18 June 2015 on the recovery and resolution of credit institutions and investment firms and through Royal Decree 1012/2015 of 6 November 2015, implementing Law 11/2015 of 18 June 2015 on the recovery and resolution of credit institutions and investment firms and amending Royal Decree 2606/1996 of 20 December 1996 on the Deposit Guarantee Scheme for Credit Institutions. The salient milestones to date have been:

Institutions within the scope of resolution regulations

The resolution framework is applicable to credit institutions, investment firms and certain financial institutions and subsidiaries of credit institutions. The Banco de España is the authority responsible for the preventive functions related to the resolution of credit institutions.

Resolution objectives

- To ensure the continuity of critical functions.

- To avoid a significant adverse effect on financial system stability, in particular by preventing contagion to the system as a whole and maintaining market discipline.

- To protect public funds by minimising reliance on extraordinary public financial support.

- To protect depositors and investors covered by the Deposit Guarantee Scheme Directive (2014/49/EU) and the Investor Compensation Scheme Directive (97/9/EC), respectively.

- To protect customer funds and assets.