Institutions are required to maintain sufficient own funds and eligible liabilities (debt instruments) to absorb losses and, if necessary, restore capital, to support the implementation of the resolution tool the authorities deem most appropriate. To do this, depending on their systemic importance and the jurisdictions where they operate, institutions must comply with a minimum requirement for own funds and eligible liabilities (MREL) and a total loss-absorbing capacity (TLAC).

What is the MREL?

The MREL is a requirement aimed at ensuring that institutions have sufficient own funds and eligible liabilities to support the application of resolution tools and make sure that shareholders and creditors are the first to bear losses should the institution fail. This requirement therefore ensures that these instruments are:

- available to absorb the losses incurred by the institution;

- capable of recapitalising the institution, if necessary;

- available to successfully apply the resolution tool.

The level of instruments available to comply with the MREL is determined for each institution or group, using calculation criteria that are pre-defined by the resolution authorities.

And the TLAC?

The TLAC is a requirement that must be met by institutions classified as global systemically important banks (G-SIBs). This requirement is similar and additional to the MREL, as it seeks to ensure that G-SIBs have sufficient own funds and eligible liabilities that can be used in the event of resolution. The MREL and the TLAC are therefore complementary elements of a common framework.

This requirement is based on an international standard for G-SIBs, namely the TLAC Term Sheet (“TLAC standard”), which was published by the Financial Stability Board on 9 November 2015 and endorsed by the G20 that same month. This standard requires G-SIBs to maintain enough high-quality loss-absorbing liabilities (usable in a bail-in) to ensure a quick and adequate loss-absorbing and recapitalisation capacity in the event of resolution. The TLAC standard was incorporated into Union law through Regulation (EU) 2019/876 of the European Parliament and of the Council of 20 May 2019.

Some of the main differences between the TLAC requirement and the MREL are listed below.

- The TLAC only applies to G-SIBs, so there are fewer institutions subject to the TLAC requirement than to the MREL

.

. - The level of TLAC is determined in advance and does not, therefore, have to be set on a periodic or case-by-case basis by the authority, as the MREL does. The TLAC is set at 18% of risk-weighted assets and 6.75% of the total exposure measure (TEM) or the leverage ratio exposure (LRE).

- There are greater eligibility requirements for TLAC purposes than for MREL purposes, with one key difference being that liabilities have to be subordinated in order to be eligible for the TLAC.

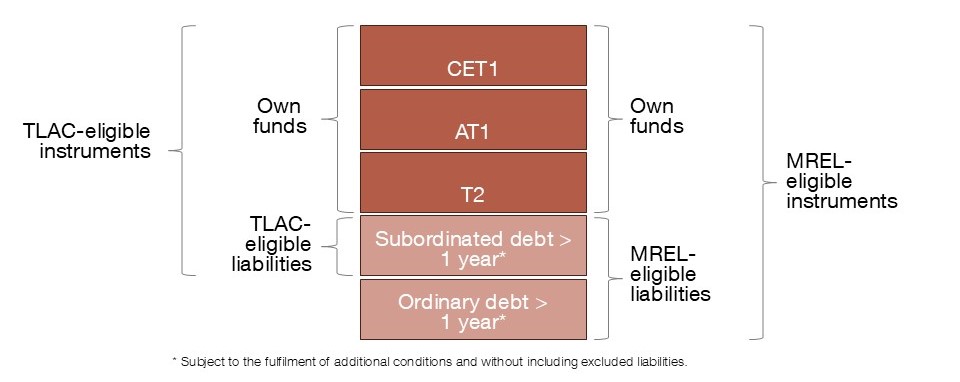

What instruments can institutions use to comply with these requirements?

To comply with these requirements, institutions must have sufficient capital (Common Equity Tier 1, Additional Tier 1 and Tier 2) and eligible liabilities (known together as eligible instruments). Only certain categories of liabilities (residual maturity of at least one year, a certain subordination level and certain other characteristics) are eligible for MREL or TLAC purposes.

The TLAC requirement must be met in full with own funds and subordinated liabilities (subordinated debt, non-preferred senior debt and other subordinated debt instruments), whereas the MREL can also be met with ordinary liabilities.

What are the specific requirements for institutions?

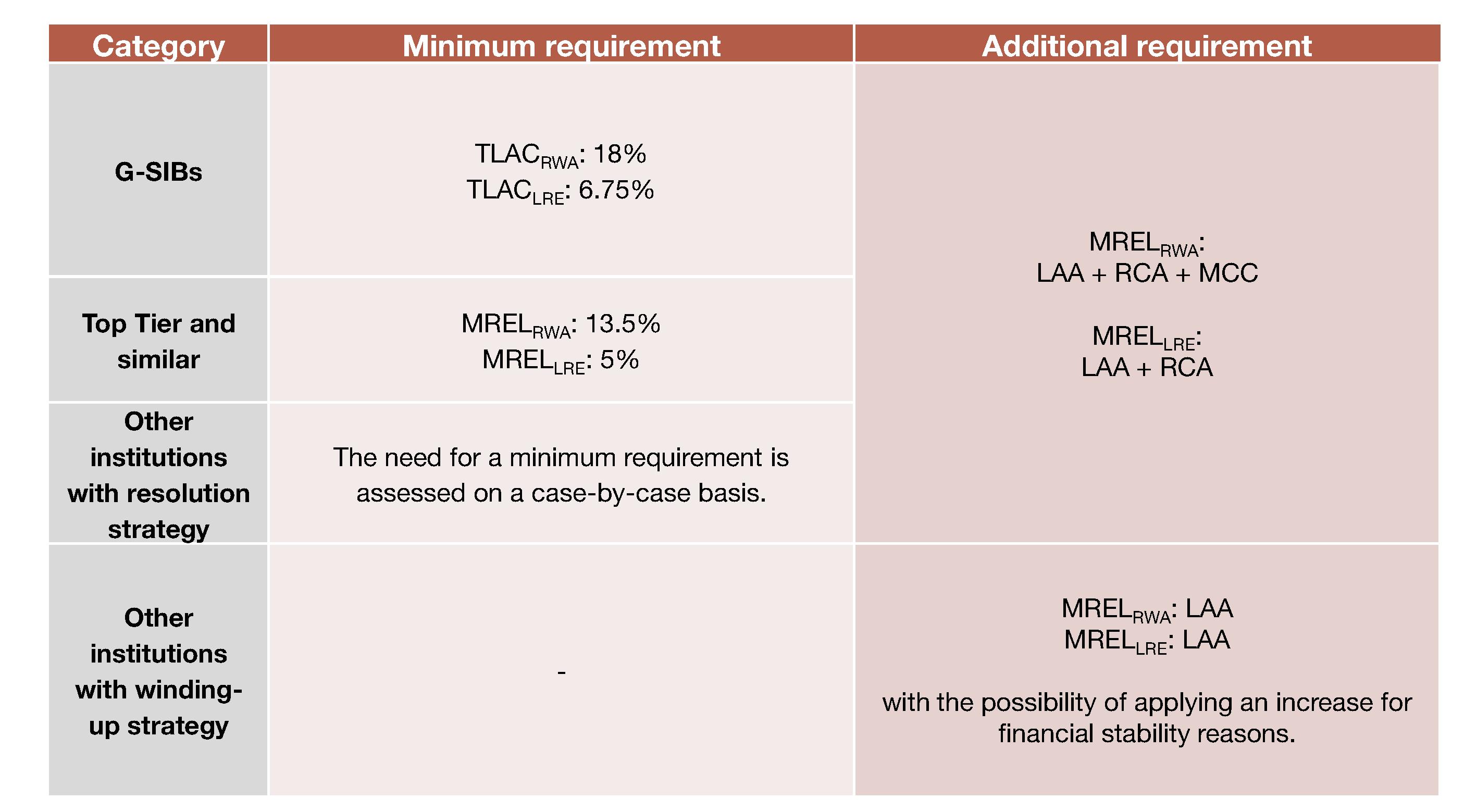

The MREL and TLAC requirements do not apply to all banking groups equally, as the specific requirements are determined according to the category of each institution. The general classification of these requirements, by category, is as follows:

RWA – risk-weighted assets; LRE – leverage ratio exposure; LAA – loss-absorption amount; RCA – recapitalisation amount; MCC - Market confidence charge.

The minimum requirement is the minimum that banking groups must maintain at all times for MREL and TLAC purposes. They are determined on a standardised basis for each category, without any differences in grading within these categories. These levels must be reached using only subordinated resources.

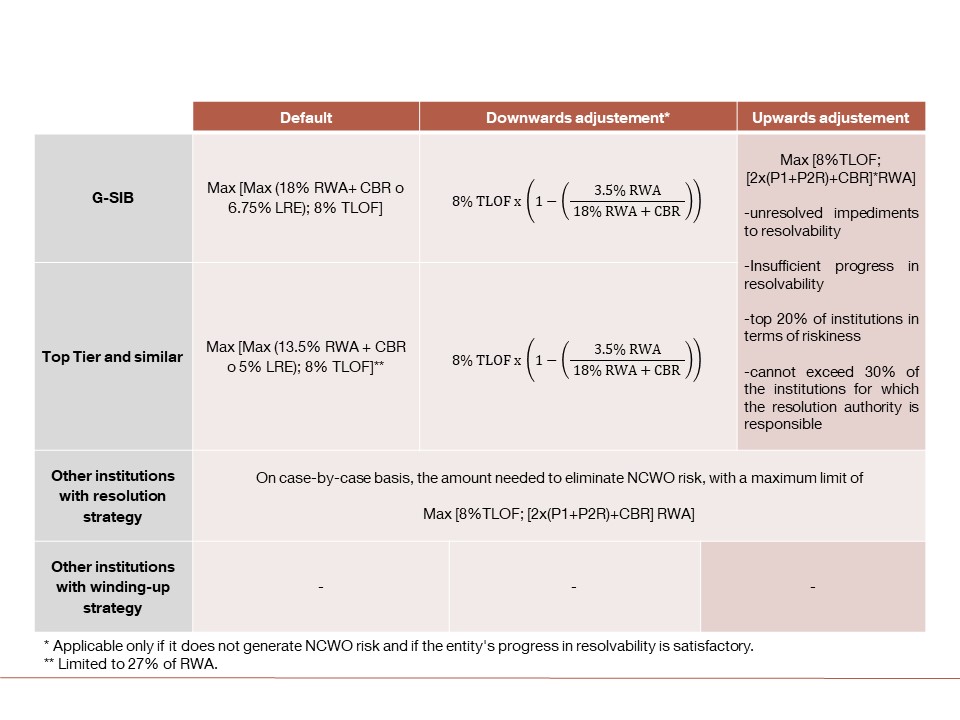

The additional requirement is an MREL requirement which is set on a case-by-case basis within each category, taking into account the specific characteristics of each banking group. A minimum amount of this specific MREL must be met with own funds and subordinated liabilities (subordination requirement). The general rule for calculating the subordination requirement is as follows:

RWA – risk-weighted assets; LRE – leverage ratio exposure; TLOF – total liabilities and own funds; CBR – combined buffer requirements; LAA – loss-absorption amount.

On top of their MREL-TREA and TLAC-TREA requirements, institutions must also meet their combined buffer requirement (not applicable in the case of the MREL-LRE and TLAC-LRE requirements).

What are the consequences of not meeting the MREL+CBR?

In addition to the minimum requirement for own funds and eligible liabilities (MREL), which is calibrated on the basis of risk-weighted assets (RWAs),1,2 institutions are also required to meet their combined buffer requirement (CBR). This is known as "CBR on top of MREL". When an institution fails to meet this additional requirement, it must immediately notify the preventive resolution authority (Article 16 bis, Law 11/2015).

In this situation, under Article 16 bis, the resolution authority can prohibit or limit the distribution of capital (M-MDA[3]) by the institution. Specifically:

- The institution may not distribute more than the M-MDA in connection with CET1 (dividends) or AT1 (interest), or assume the obligation to pay variable remuneration or discretionary pension benefits, or make such payments if it had already assumed these obligations in a situation where it failed to meet the MREL+CBR.

- The method for calculating this limit (M-MDA) is identical to that used for the MDA relating to solvency.

- The resolution authority, after consulting the competent supervisor, shall assess whether to exercise this power taking into account the reason, duration and magnitude of the failure to comply and its impact on resolvability, the institution’s financial situation, etc. It shall make this assessment at least every month for as long as the institution fails to meet the requirements.

- If the resolution authority finds that the institution still fails to meet its “CBR on top of MREL” nine months after it has notified that situation, the preventive resolution authority, after consulting the competent supervisor, shall exercise the power to limit distributions, unless it applies a well-founded exception on the grounds that there is a serious disturbance in the financial markets that prevents the institution from issuing instruments or the prohibition would lead to negative spill-over effects for part of the banking sector, thus potentially undermining financial stability.

What are the consequences of not meeting the MREL?

Article 86 of Royal Decree 1012/2015, implementing Law 11/2015, establishes that any failure to meet the MREL requirement, either in terms of RWAs or LRE, shall be dealt with by the competent supervisor or the preventive resolution authority, as appropriate, bearing in mind at least one of the following elements:

- The powers to address impediments to resolvability, as set out in Articles 17 and 18 of Law 11/2015.

- The power to prohibit certain distributions of capital, as set out in Article 16 bis of Law 11/2015 (the above-mentioned M-MDA).

- The supervisory powers set out in Article 69 of Law 10/2014.

- The early intervention measures set out in Article 9 of Law 11/2015.

- The administrative penalties referred to in Chapter IX (sanctioning regime) of Law 11/2015.

In addition, the competent authority4 shall assess whether the institution is “failing or likely to fail (FOLTF)”.5

The resolution authority and the competent supervisor shall consult with each other if they decide to exercise the above-mentioned powers.

Powers to address impediments to resolvability

Under Law 11/2015, these powers shall be exercised when there are substantive impediments to the resolution of an institution. These powers would include the following, to name a few:

- Limiting the individual and aggregate exposures of the institution;

- Requiring the institution to divest specific assets or limit or cease specific activities;

- Restricting or preventing the development of specific business lines or sale of specific products;

- Requiring changes to the legal and operational structure of the institution;

- Requiring the institution to submit a plan to restore compliance with the MREL requirement; or

- Requiring an institution to issue eligible liabilities to meet the MREL requirement.

Supervisory powers

Provision is made for the supervisor to impose Pillar 2 prudential measures, when deemed appropriate.

Early intervention measures

These include the following, to name a few:

- Requiring the management body of the institution to implement one or more of the measures set out in its recovery plan within a set timeframe or to update the plan, or examine the situation, identify the measures needed to address any problems detected and draw up an action plan to overcome those problems;

- Requiring one or more members of the management body, general managers and other similar officers to be removed or replaced if those persons are found unfit to perform their duties pursuant to the suitability requirements;

- Requiring changes to the legal or operational structures of the institution or of the consolidated group or subgroup;

- If the aforementioned measures are not sufficient, agreeing to appoint one or more administrators, or to temporarily replace the institution’s management body or one or more of its members.

Administrative penalties

Failure to meet the MREL requirement may be classified as a very serious, serious or minor infringement:

- Very serious infringements entail a failure to cover the MREL for at least six months and falling below 80% of the minimum requirement (Article 79(r) of Law 11/2015).

- Serious infringements also entail a failure to cover the MREL for at least six months, but the quantitative requirement is inconsequential (Article 80(r) of Law 11/2015).

- Minor infringements entail breaches that do not constitute either very serious or serious infringements (Article 81 of Law 11/2015). Thus, any failure to meet the MREL requirement in such cases, irrespective of quantitative or time factors, would constitute a minor infringement.

The penalties for very serious, serious or minor infringements are set out in Articles 83, 84 and 85, respectively, of Law 11/2015.

1RWAs are also referred to as TREA (total risk exposure amount).

2MREL must be met in terms of both RWAs and leverage ratio exposure (LRE).

3Maximum distributable amount related to MREL.

4The authority that has to determine whether an institution is failing is the competent supervisor. However, the Single Resolution Board may determine whether an institution is failing or likely to fail when it has required the European Central Bank to make such an assessment and the latter has not done so within three days (the Spanish executive resolution authority (FROB) may require the Banco de España to declare the failure of an institution, but it cannot do so on its own).

5An institution is deemed to be failing if any of the following circumstances prevail or are close to doing so: a) the institution infringes, or there are objective elements indicating that it will in the near future infringe, the solvency or other requirements for continuing authorisation; b) the institution’s assets are less than its liabilities; c) the institution is unable to pay its debts or other liabilities as they fall due; d) extraordinary public financial support is needed (with some exceptions)..