The Banco de España can impose limits and conditions on lending, such as maximum loan amount depending on the collateral provided or the borrower’s income, and the maximum loan term. They are a means of avoiding borrowers' creditworthiness becoming impaired.

They are not intended to replace the credit standards established by banks themselves, but rather to establish sufficiently prudent conditions when a widespread easing of those standards might pose a threat to financial stability.

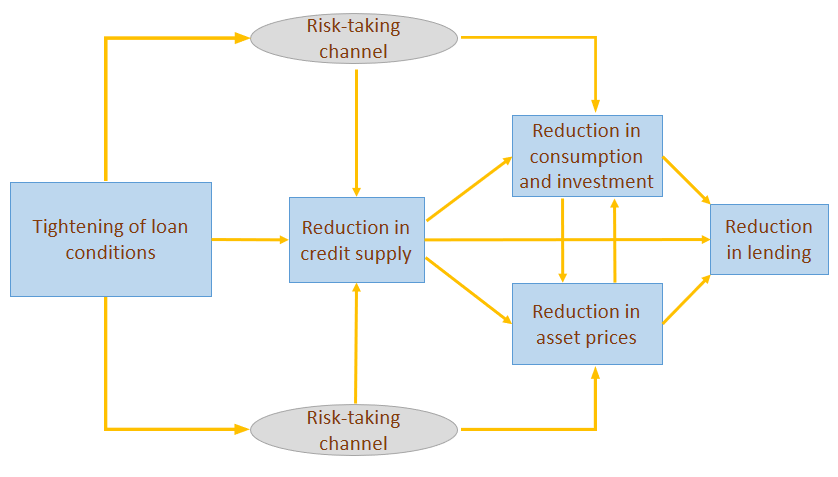

As depicted in the diagram, the tightening of lending conditions makes banks take actions (e.g. reduce the supply of credit, take on less risk) that moderate the economic cycle (consumption and investment) and financial asset prices. This, in turn, also moderates the credit cycle.

Note: See A. Estrada and J. Mencía (2021), "El cuadro de mandos de la Política Macroprudencial![]() ”, Información Comercial Española, No 918, 2021. (Only available in Spanish).

”, Información Comercial Española, No 918, 2021. (Only available in Spanish).

The conditions are only applied to new loans. Therefore, they are ineffective against the financial stability impact of existing loans extended under excessively loose conditions.

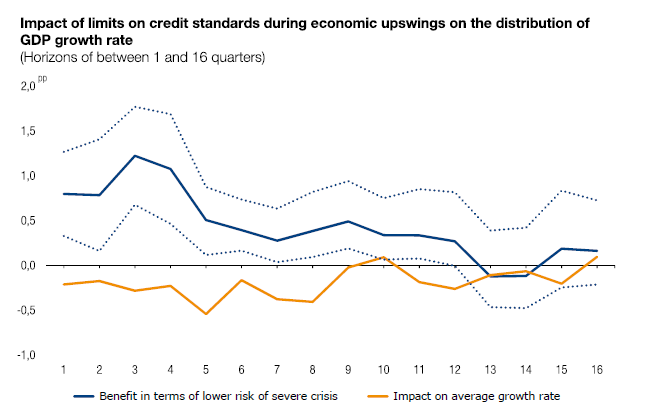

The following chart suggests that, when applied during an upswing at the first sign of a widespread and excessive easing of credit standards, these tools immediately reduce the likelihood of steep drops in GDP.

Note: The continuous blue and yellow lines represent the estimated impact in percentage points on the 5th and 50th percentile of the conditional distribution of GDP growth, respectively. The dotted blue lines represent the bands at 95% confidence. The analysis is carried out for a sample of 28 EU countries. For details of the methodology, see Galán J.E. (2020). The benefits are at the tail: uncovering the impact of macroprudential policy on growth-at-risk![]() . Journal of Financial Stability, in press.

. Journal of Financial Stability, in press.

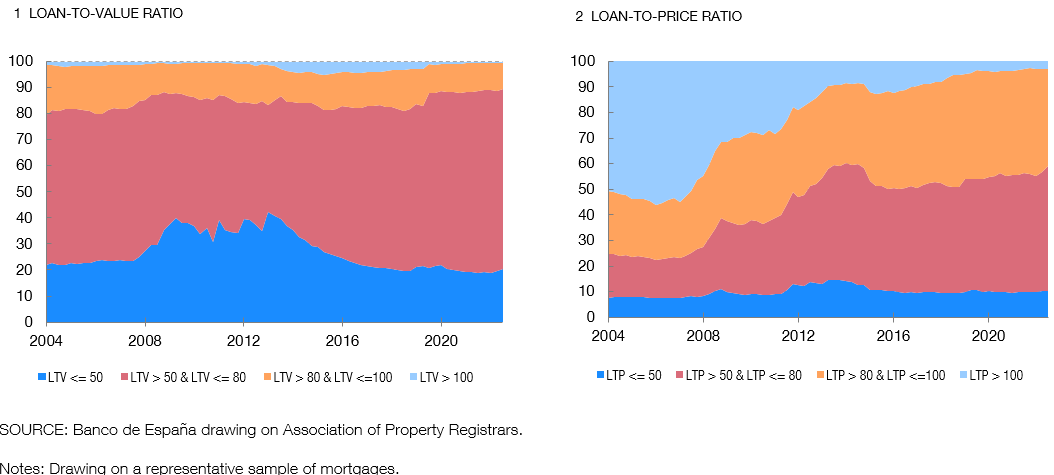

Some examples of charts monitoring credit standards

The loan-to-value (LTV) ratio is the ratio of the mortgage loan’s principal to the appraised value of the property. The loan-to-price (LTP) ratio is the ratio of the mortgage loan’s principal to the price of the property recorded in the sale. Both ratios are calculated for each mortgage on origination of the loan.

The charts depict the distribution of the two ratios over time. Higher values in either ratio denote an easing of credit standards (higher risk). Since 2008 there has been an ongoing decline in the proportion of mortgage loans with values for LTV and LTP above 80%. In the wake of the outbreak of the pandemic in 2020, the proportion of riskier mortgage loans (with values for LTV and LTP above 100%) has held steady.