What does responding “I don't know” say about your gender and your financial literacy and behaviour?

The differences between men and women in financial literacy do not depend solely on whether their replies to a survey are right or wrong. Women tend to respond “I don’t know” more frequently. This option, which helps to explain the gender gap in literacy, is also linked to specific financial behaviours and settings.

International Women’s Day is celebrated on 8 March. In economics we often talk about differences between men and women![]() in employment

in employment![]() , promotions

, promotions![]() or wages. But there is another gender gap that also influences well-being: the gender gap in financial competences. Aside from the different ways in which men and women save, invest and use insurance products, there are also

or wages. But there is another gender gap that also influences well-being: the gender gap in financial competences. Aside from the different ways in which men and women save, invest and use insurance products, there are also![]() significant differences in financial knowledge.

significant differences in financial knowledge.

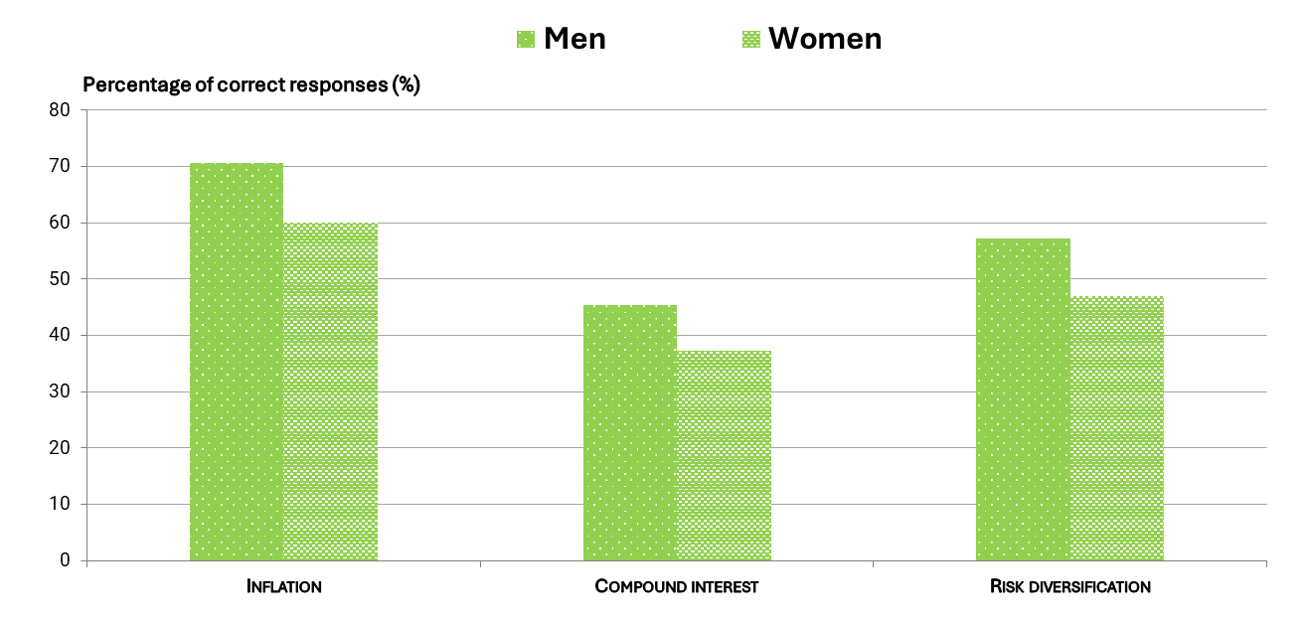

Men respond correctly to more financial questions than women

In Spain and in many other countries![]() women have, on average, lower levels of financial literacy than men. Financial literacy is measured very simply as the percentage of correct answers to basic questions about concepts such as inflation, compound interest and risk diversification (Chart 1).

women have, on average, lower levels of financial literacy than men. Financial literacy is measured very simply as the percentage of correct answers to basic questions about concepts such as inflation, compound interest and risk diversification (Chart 1).

Chart 1

FINANCIAL LITERACY IN SPAIN, BY GENDER

PERCENTAGE OF CORRECT RESPONSES RELATING TO BASIC CONCEPTS

SOURCE: Devised by authors based on microdata from the 2021 Survey of Financial Competences.

What's behind the differences?

Part of the gender gap in the percentage of correct answers is explained![]() by differences in observable characteristics between men and women, such as differences in educational level, numerical/reading skills, interest or experience in finance, specialisation in housework, confidence and other institutional or cultural factors, like social norms. When we compare men and women with the same educational level, numerical/reading skills, interest and experience in finance, etc., they have a similar share of correct responses but men still get more answers right.

by differences in observable characteristics between men and women, such as differences in educational level, numerical/reading skills, interest or experience in finance, specialisation in housework, confidence and other institutional or cultural factors, like social norms. When we compare men and women with the same educational level, numerical/reading skills, interest and experience in finance, etc., they have a similar share of correct responses but men still get more answers right.

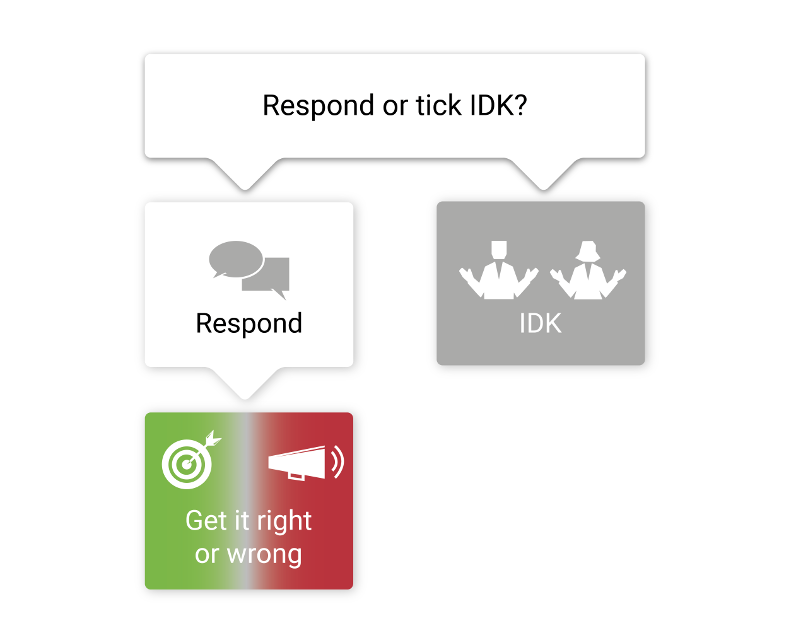

Let's have a look at how we measure this. The standard financial literacy index is based on the proportion of correct answers relative to the total, i.e. only correct answers are counted. But the results of the survey can provide more information, namely that contained in the incorrect answers, which arise from two different decisions (Figure 1).

- Choosing to respond and making a mistake

- Choosing the “I don't know” (IDK) option

Figure 1

DOUBT MANAGEMENT

NOTE: IDK stands for I don´t know

SOURCE: Devised by authors.

In the first case, the result is an error which clearly reflects a lack of knowledge. However, the IDK option doesn’t reveal whether there is a lack of knowledge (they don’t know the answer) or there is another reason, such as a lack of confidence (when in doubt, they choose the IDK option).

Surveys usually detect gender differences: women generally opt for IDK more often than men. However, we can’t say whether this is because more women don’t know the answer or because they are more cautious or less confident. We'll analyse whether this difference goes beyond a lack of knowledge.

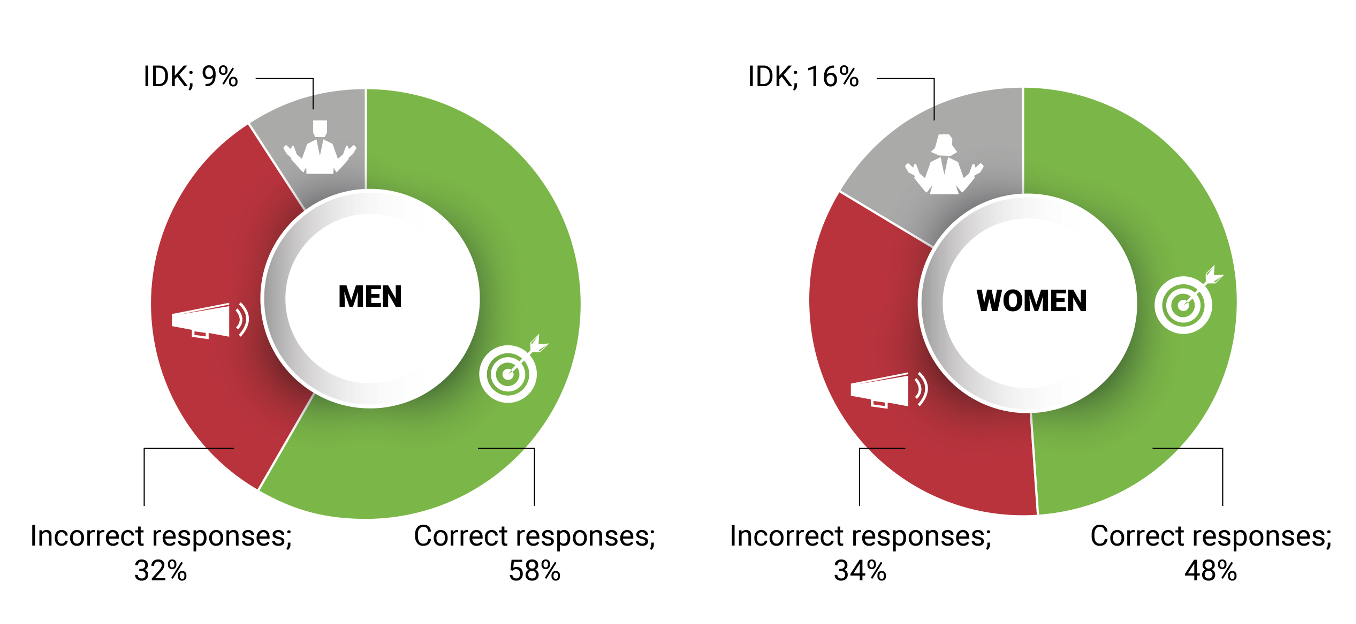

Also important is how often IDK is used to respond

In practice, it has been documented that in many countries there is also a gender gap in the probability of responding IDK. Spain is no exception: women choose this option nearly twice as often as men (Chart 2).

Chart 2

RESPONSES IN THE SURVEY OF FINANCIAL COMPETENCES, BY GENDER

SOURCES: 2021 Survey of Financial Competences![]() .

.

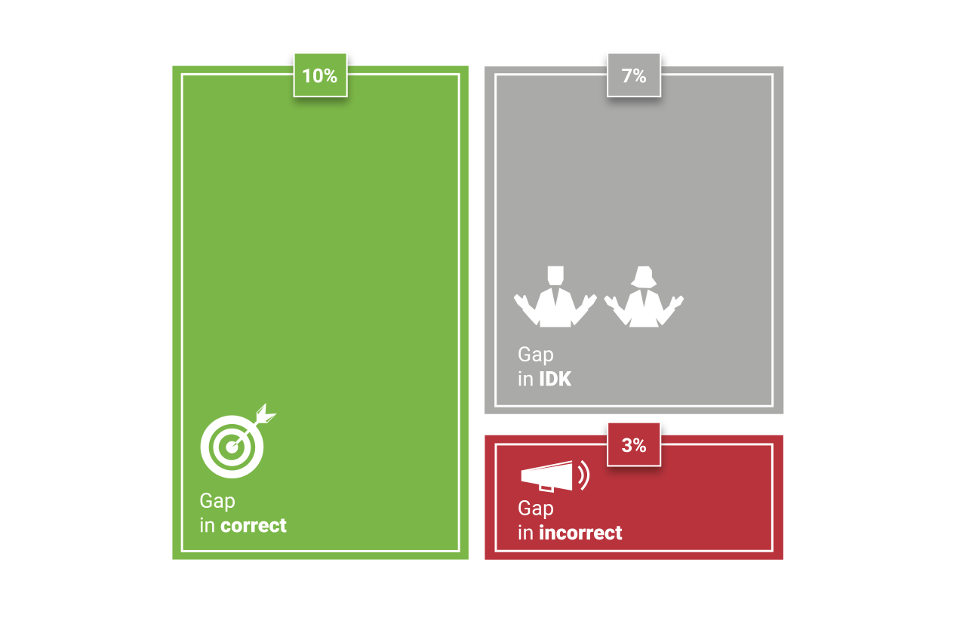

The gender gap in financial knowledge is divided into one part that is attributable to incorrect answers and another that relates to women’s greater propensity to respond IDK

Actually, the differences between men and women in choosing the IDK option are greater than the differences in incorrect responses (Chart 3). Based on microdata![]() from the 2021 Survey of Financial Competences

from the 2021 Survey of Financial Competences![]() we show that the gender gap when responding IDK (7%) is equivalent to two-thirds of the differential in correct answers (10%) to questions on inflation, compound interest and risk diversification.

we show that the gender gap when responding IDK (7%) is equivalent to two-thirds of the differential in correct answers (10%) to questions on inflation, compound interest and risk diversification.

Chart 3

GENDER GAPS IN RESPONSES

Sources: 2021 Survey of Financial Competences![]() .

.

Answering IDK isn’t just a lack of knowledge, it’s also a pattern of behaviour (and it’s malleable)

While researching the possibility of gleaning information from surveys other than responses in the form of numerical data, in another study![]() we show that the frequency of respondents with similar literacy levels choosing the IDK option may vary if aspects of the survey design are changed.

we show that the frequency of respondents with similar literacy levels choosing the IDK option may vary if aspects of the survey design are changed.

We conducted an online survey based on the questionnaire used for the Survey of Financial Competences and the guidance of the OECD International Network on Financial Education![]() but we randomly changed – most importantly – the design of the section on questions about financial knowledge in three ways by:

but we randomly changed – most importantly – the design of the section on questions about financial knowledge in three ways by:

- Removing the IDK option.

- Providing monetary incentives for correct answers.

- Including an “informational nudge”, where we ask respondents to avoid choosing IDK and we indicate that a large part of the knowledge gap between men and women is attributable to women choosing the IDK response more frequently.

This is how we reduced IDK responses significantly in both genders and with the informational nudge, much more for women, where the gender gap was halved. We thus conclude that IDK is not always a fixed response and, therefore, it does not unequivocally indicate a lack of knowledge. It is also linked to a pattern of behaviour.

The informational nudge manages to change it and to reduce the gender gap in IDK, a gap that can even be closed once other population characteristics are controlled for in regression models. Let’s continue.

What else does IDK tell us?

So far, choosing IDK could seem “merely” a measurement problem or an issue relating to different behaviours in surveys. However, choosing IDK also reveals important aspects of individuals’ well-being.

In our research![]() we show that selecting the IDK option is related to findings in other standard indicators of financial competences

we show that selecting the IDK option is related to findings in other standard indicators of financial competences![]() . The higher the number of IDK responses, the worse the results in indicators of financial behaviour, objective financial well-being, awareness and holding of financial products, even when comparing responses across individuals with similar financial literacy levels.

. The higher the number of IDK responses, the worse the results in indicators of financial behaviour, objective financial well-being, awareness and holding of financial products, even when comparing responses across individuals with similar financial literacy levels.

More IDK responses are linked to poorer results in measures of financial health, patterns of financial behaviour and awareness and holding of financial products.

DID YOU KNOW ...?

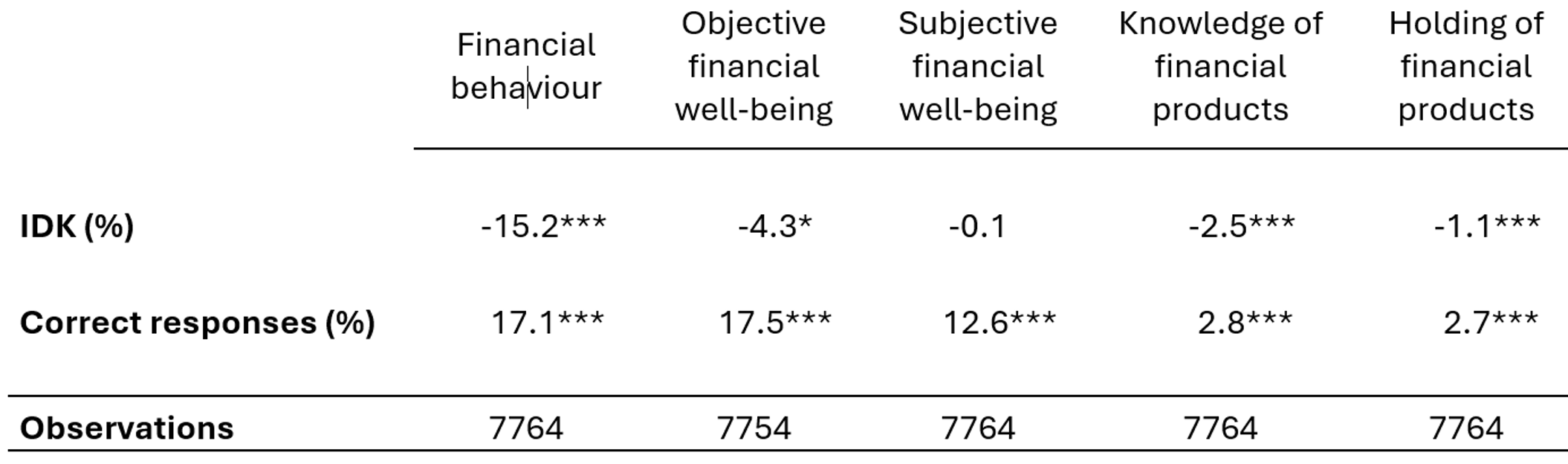

In our![]() analysis we use the 2021 Survey of Financial Competences to study the correlation between responding IDK and other financial findings. We find that a higher percentage of IDK responses in questions about financial knowledge is linked to poorer financial indicators, even when comparing individuals with the same percentage of correct responses in questions about financial literacy.

analysis we use the 2021 Survey of Financial Competences to study the correlation between responding IDK and other financial findings. We find that a higher percentage of IDK responses in questions about financial knowledge is linked to poorer financial indicators, even when comparing individuals with the same percentage of correct responses in questions about financial literacy.

The numbers in the table show the correlation with each financial indicator. Thus, for example, a one percentage point (pp) increase in IDK responses is linked to 15 pp less in the financial behaviour index.

Link between IDK and financial indicators

NOTE: The asterisks (*) indicate that this correlation is statistically significant with a probability of 99% (***), 95% (**) and 90% (*). The regression also includes a gender indicator variable.

SOURCE: Hospido, Iriberri, Machelett (2025), based on data from the 2021 Survey of Financial Competences.

The financial indicators which we use are:

- Financial behaviour. Measured by eight practices: keeping track of money, actively saving, not borrowing to make ends meet, seeking advice, monitoring personal finances, setting long-term goals, making considered purchases and paying bills on time.

- Objective financial well-being. Ability to cope with shocks (measured by having sufficient income to cover expenses in the last 12 months; and, if the main source of income had been lost, covering expenses without borrowing or moving for at least three months).

- Subjective financial well-being. Being satisfied with their financial situation, feeling that their financial situation does not limit their ability to do what is important and not having too much debt.

- Financial product knowledge: sum of being aware of payment, saving/investment products, insurance products, credit products and crypto products.

- Holding of financial products: sum of individual and joint holding of payment, saving/investment products, insurance products, credit products and crypto products.

On 8 March this year, measuring the financial gap also means paying attention to the IDKs. The behavioural component of that gap can be modified. For that reason, our agenda includes highlighting it so that fewer women feel that they haven’t got a clue about finance and more of them can respond, participate and confidently decide about their present and future financial well-being.

DISCLAIMER: The views expressed in this blog post are those of the author(s) and do not necessarily coincide with those of the Banco de España or the Eurosystem.