Financial education from an early age: an investment that pays off

Learning about money from a young age helps us develop a critical and responsible mindset and prepares us for the financial decisions we will face as adults. This is what financial education seeks to offer children and young people, going far beyond simply teaching financial concepts.

6 min.

Although talking to children about money can feel premature, the fact is that they start making financial decisions at a very young age, like what to spend their pocket money on or how much to put in the piggy bank. Our early experiences with money can form lasting attitudes that will affect how we manage our finances later in life. This is why learning how to manage money from an early age is essential and one of the goals of financial education, to which the Banco de España is deeply committed.

What should financial education focus on for children and young people? Who should be responsible for guiding our children in their early learning? And how ready is Spain to meet this challenge?

How to introduce financial education at a young age

Early on, financial education![]() :

:

- teaches children very basic, but important, financial concepts

- encourages them think about how they use their money and

- ensures that they develop habits and attitudes that enable them to take the appropriate economic and financial decisions in any situation, such as thinking before spending and knowing the difference between what they need and what they want.

Financial education teaches children and young people the basic concepts, attitudes and habits that will help them make wise economic and financial decisions

Step by step

Financial education should be a natural part of everyday life, adapted to each age group and situation and introduced gradually (Photo gallery 1).

Children learn by playing, exploring and experiencing everyday situations. By talking to them about money in a natural way and involving them in simple planning tasks (like making a shopping list) or encouraging them to have simple saving goals (such as buying a toy or taking part in an interesting activity), we will be helping them build financial habits for the future.

We can also encourage attitudes such as spending wisely or feeling good about sharing or giving some of their money to others. We can even teach them simple financial concepts, helping them to understand the value of money.

Photo gallery 1 click to zoom

LEARNING SCENARIOS

SOURCE: Devised by authors

As children grow older and become teenagers, they will be able to:

- understand basic financial tools, such as what a bank account is and how digital banking works, how to protect themselves from fraud and financial scams and ways to save and plan for the future;

- grasp more complex financial concepts such as inflation, interest rates and what they mean for saving. This is when they start thinking about their future career choices –employment– in terms of what they might earn –wages–and the long-term prospects;

- cultivate attitudes, such as knowing their rights and responsibilities as consumers and bank customers, having a critical approach to advertising and marketing messages, and using digital payment tools and money responsibly.

Financial education should be part of everyday life, adapted to each situation and introduced gradually

Who is responsible for teaching children and young people about money? Each one’s key role

As we have seen, financial education must be integrated into everyday life and tailored to each age. Schools, families and other social actors must therefore work closely together to achieve this. It is a shared responsibility, not the task of one institution alone (Figure 1).

Figure 1 click to see what each can do

A SHARED RESPONSIBILITY

SOURCE: Devised by authors

At home, we learn about money almost without realising it when we see how adults save and organise their spending. This is perhaps the best environment for us to take our first steps managing our money, learning directly from our parents. This is increasingly what is happening, as the old taboo around talking about money at home gradually falls away.

That said, the educational authorities also have a crucial role to play, laying out a financial education framework tailored to each stage of learning. In schools, the challenge is to design programmes that actually work. The most effective programmes strike a balance between theory and practice. They use games, role-play, group activities and, above all, conversations rooted in real-life situations that show why these topics matter. Knowledge alone is not enough. Healthy attitudes to money also need to be developed. There is little benefit in explaining the value of saving to children without helping them to build lasting habits or curbing impulsive behaviour.

Other educational settings (public or private institutions, such as banking associations, ministries, central banks and supervisory authorities) also have an important role to play, sharing financial knowledge and habits in a clear and structured way. Regardless of the setting, for educational programmes to be effective they must be tailored to the learner's age, stage of development and circumstances.

And what about Spain?

In the Spanish education system, financial education![]() has expanded its presence in schools. The current law on education governing primary and secondary schooling weaves the topic into various compulsory and optional subjects across the curriculum: mathematics

has expanded its presence in schools. The current law on education governing primary and secondary schooling weaves the topic into various compulsory and optional subjects across the curriculum: mathematics![]() , entrepreneurship and natural and social sciences and humanities, for example.

, entrepreneurship and natural and social sciences and humanities, for example.

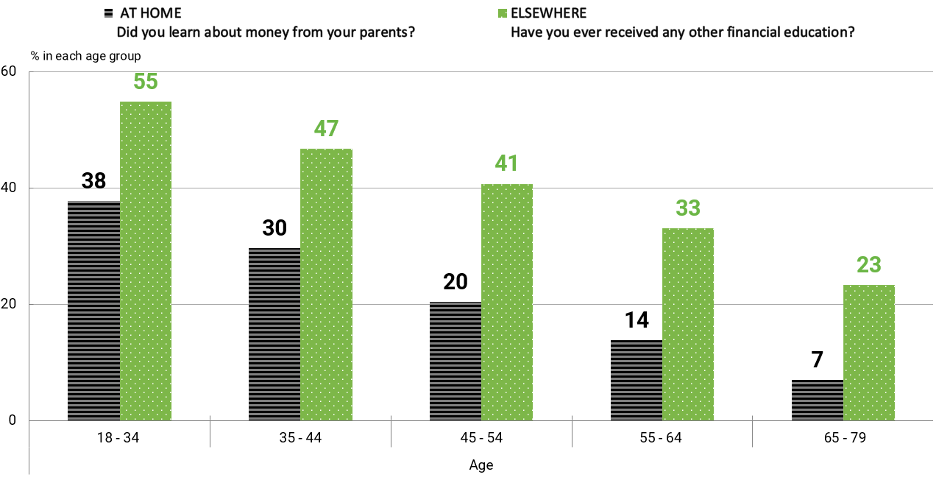

What do the data say? The share of people who receive financial education both at home and elsewhere has been growing from one generation to the next (Chart 1).

Chart 1

PROPORTION OF PEOPLE IN SPAIN, BY AGE GROUP, WHO REPORT HAVING RECEIVED SOME FORM OF FINANCIAL EDUCATION

SOURCE: Survey of Financial Competences![]() (2020-2021)

(2020-2021)

NOTE:

- Financial education at home: as reported by each age group in relation to their childhood and early life

- Financial education elsewhere: across all ages and environments including primary and secondary school, vocational training, university, the workplace, voluntary courses or self-learning.

Even so, the results of the latest PISA![]() assessment (2022)

assessment (2022)![]() show that Spanish students score below the OECD average in financial literacy, and that there has been no significant improvement over the past decade.

show that Spanish students score below the OECD average in financial literacy, and that there has been no significant improvement over the past decade.

This points to the need for a greater effort from national institutions committed to financial education, including the education community itself. That means training teachers, giving them the right tools and continuing to add financial education content to the school curriculum. Only then can we ensure that everyone has access to a basic level of financial education. The results of all this will be even better if families are actively involved as well.

A greater effort is needed: training teachers, giving them the right tools and continuing to expand financial education content within the school curriculum. And families need to be actively involved

The Banco de España: committed to financial education

The Banco de España![]() , within the European Union and the OECD, has helped to develop a financial competence framework for children and young people

, within the European Union and the OECD, has helped to develop a financial competence framework for children and young people![]() . This framework sets out the skills that should be acquired at each stage of development and serves as a key reference point for future changes to education law at both national and regional level.

. This framework sets out the skills that should be acquired at each stage of development and serves as a key reference point for future changes to education law at both national and regional level.

We are currently developing a new strategic approach to financial education with a stronger commitment to children and young people. The focus is on educational centres, on resources and content, and on teacher training.

DID YOU KNOW ...?

Our new strategy:

- promotes financial education in schools;

- includes the design of content and resources;

- prioritises teacher training. It shifts the emphasis from teaching students to training teachers, so that they can pass on the content effectively and adapt it to the needs of their pupils;

- fosters institutional partnerships to strengthen financial education from the earliest levels of education. We are building alliances with regional education authorities

and with universities;

and with universities; - introduces rigorous systems to measure and track success, allowing us to ensure the quality and impact of programmes and drive continuous improvement;

- includes plans to set up financial education centres within the Banco de España’s branch network.

Investing in sound, age-appropriate financial education from an early age means preparing new generations to be informed consumers and more aware as citizens. Teaching them how to think about and make financial decisions is one of the best investments we can make as a society and one that pays off. Here at the Banco de España, there is no doubt of that.

DISCLAIMER: The views expressed in this blog post are those of the author(s) and do not necessarily coincide with those of the Banco de España or the Eurosystem.