Financial inclusion of immigrants: the banking barrier for those in an irregular situation

Financial inclusion is a key part of immigrants’ integration. Overall, there is no significant financial inclusion gap between immigrants and the Spanish-born population. The exception is immigrants in an irregular situation, for whom opening a bank account is often an insurmountable barrier, leaving them financially excluded.

Immigration has increased markedly in recent years. Today, one in five people living in Spain was born abroad. Integrating immigrants is not only a major social challenge, but also an economic one. It’s key if they are to realise their full potential and maximise their contribution to growth in their host country. Financial inclusion is at the heart of this process, as it encourages greater income stability, enables saving and makes credit more easily available. In our Financial Inclusion Report![]() , we examine this issue, distinguishing between the immigrant population as a whole and those who have arrived more recently and, in particular, those in an irregular situation. This latter group faces, by far, the greatest hurdles to financial inclusion. How does the financial situation of immigrants compare with that of people born in Spain? What risk of financial exclusion do they face and how can it be reduced?

, we examine this issue, distinguishing between the immigrant population as a whole and those who have arrived more recently and, in particular, those in an irregular situation. This latter group faces, by far, the greatest hurdles to financial inclusion. How does the financial situation of immigrants compare with that of people born in Spain? What risk of financial exclusion do they face and how can it be reduced?

Financially speaking, immigrants do not differ markedly from the Spanish-born population

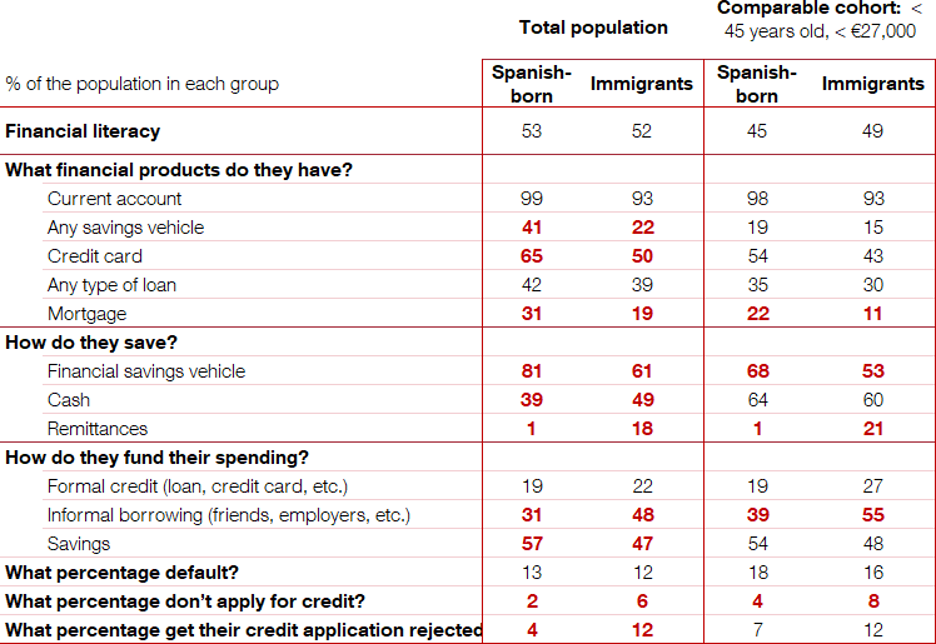

We are defining immigrants as people that live in Spain who were not born here. Comparing them with the Spanish-born population allows us to identify areas where they may face a higher risk of financial exclusion. This analysis is possible by drawing on data from the 2021 Survey of Financial Competences![]() .

.

When comparing like this, it’s important to account for the fact that the immigrant population differs in certain ways from the Spanish-born population, affecting the outcome. We’re therefore using two benchmarks: the overall populations of people born in Spain and immigrants, and subgroups with similar age and income profiles. The latter helps control, at least in part, for the impact of socioeconomic differences.

DID YOU KNOW ...?

-Immigrants are, on average, younger than the Spanish-born population (41 versus 45 years old), although their average age has been increasing. In any event, the percentage of older people is lower: only 3% are over 74, compared with 12% among those born in Spain.

-Income levels are also lower: in 2021 46% of immigrant households had an annual income below €15,000, compared with 25% of households headed by someone born in Spain.

-The comparable cohorts of the immigrant and Spanish-born populations used in this analysis consist of those under the age of 45 whose annual household income was below €27,000. In 2021, these groups represented 43% of the immigrant population, compared with 19% of the Spanish-born population.

While their financial behaviours are somewhat different, there is no financial inclusion gap between the immigrant population and those born in Spain

Across most of the indicators in Table 1, immigrants don’t differ markedly from those born in Spain, particularly when comparable cohorts are considered.

- Financial literacy is somewhat higher among those born in Spain, but that gap vanishes when we compare migrants with people born in Spain that are younger and have lower incomes.

- Only 1% of the Spanish-born population, but 7% of immigrants, are unbanked.

That said, some differences are pronounced and persist even between the comparable cohorts.

- The most notable is that nearly 20% of the immigrant population send money abroad in remittances, while very few of those born in Spain do.

- Fewer immigrants have credit cards: about half have them, compared with 65% of the Spanish-born population.

- Many of those born in Spain make use of financial products for saving (81%), but this percentage is significantly lower among immigrants (61%). By contrast, informal borrowing (from friends or employers) is more common among immigrants (48%, compared with 30% among the Spanish-born population).

- Lastly, immigrants are less likely to apply for credit and report higher rejection rates when they do so.

Table 1

DIFFERENCES IN THE FINANCIAL BEHAVIOUR OF IMMIGRANTS VERSUS THOSE BORN IN SPAIN

SOURCE: 2021 Survey of Financial Competences![]() , Banco de España.

, Banco de España.

NOTES:

-2021 data.

-The most significant differences are highlighted bold red.

-Financial literacy: average correct answers to the three questions posed for its assessment (about inflation, interest rates and long-term planning).

-The questions about how they fund their saving and spending refer to households that save and those whose outgoings exceeded their income in the previous year, respectively.

Taken together, these findings don’t point to a clear gap in terms of financial inclusion that can be attributed solely to being an immigrant. However, lower average income levels among immigrants may increase their risk of exclusion.

But irregular immigrants do face a severe barrier to banking access

The picture changes when we focus on recent arrivals, and in particular those in an irregular administrative situation. As noted above, access to a bank account is almost universal in Spain, including among immigrants. This is not the case, however, for irregular immigrants.

However, most irregular immigrants do face a significant barrier to financial inclusion: they can’t open a bank account

In the report![]() , we offer an indicative estimate of their level of access to banking services, summarised in Figure 1.

, we offer an indicative estimate of their level of access to banking services, summarised in Figure 1.

Figure 1

ACCESS TO BANKING SERVICES AMONG IRREGULAR INMIGRANTS IN SPAIN (2025)

SOURCES: Banco de España and Funcas (2026)![]()

NOTE: Immigration data refer to 1, January 2025 and those of basic payment accounts to 31, December 2024.

First, we use a range for the size of the irregular immigrant population based on estimates by Funcas![]() , as there is no official record. At the beginning of 2025, Spain was estimated to have between 614,000 and 838,000 irregular immigrants.

, as there is no official record. At the beginning of 2025, Spain was estimated to have between 614,000 and 838,000 irregular immigrants.

Second, we consider the number of basic payment accounts, one of whose main purposes is to facilitate access to banking services for vulnerable groups. By early 2025, around 83,000 such accounts had been opened with Spanish banks.

DID YOU KNOW ...?

Basic payment accounts are subject to specific legislation. Account holders can use them for simple bank transactions, such as paying in and withdrawing money and making transfers. Find out more here![]() .

.

They are intended to ensure universal access to basic financial services (a right recognised by the European Union), especially for the vulnerable and those at risk of financial exclusion.

All Spanish credit institutions are required to offer a basic payment account. Individuals without residence permits can even open one provided they have the documentation required by law to prove their identity![]() .

.

At the beginning of 2025 the best case scenario was one basic payment account for every eight irregular immigrants. While it may be true that some of those immigrants have opened another type of bank or payment account, they presumably represent a small proportion of them. People from other vulnerable groups can also open basic payment accounts. These data suggest that a majority of irregular immigrants do not have a bank account, in other words, they are unbanked.

Why can’t most irregular immigrants open a bank account?

Banks open very few basic payment accounts, despite the legislation being designed so that vulnerable groups can open them. Even if they have the documents to prove their identity, irregular immigrants are generally not well informed, which poses another obstacle to exercising their rights.

Banks’ main argument for not opening these accounts is anti-money laundering legislation, which establishes some identification requirements. It is often hard for irregular immigrants – particularly those from certain countries – to fulfil these requirements. Opening an account for this type of customer has a high operational and reporting cost and could pose the bank significant risks (sanctions or damage to its reputation) if the account is used for money laundering-related activities.

What can be done to improve the situation?

From a financial authority standpoint, the Banco de España regularly reminds![]() banks that they should consider the principle of proportionality when applying legislation so that they are more flexible in matters related to the financial inclusion of vulnerable groups. The EU’s new anti-money laundering legislation

banks that they should consider the principle of proportionality when applying legislation so that they are more flexible in matters related to the financial inclusion of vulnerable groups. The EU’s new anti-money laundering legislation![]() conveys a similar message.

conveys a similar message.

Some banks have designed specific accounts for vulnerable groups. The transactions performed with these accounts are limited, meaning they sidestep the regulatory risks.

All in all, the immigrant population integrates – and this is true from a financial perspective as well – over time, above all upon receiving their residence permit. However, most irregular immigrants face a problem, namely that they cannot open a bank account, which has knock-on effects on their day-to-day. The legalisation under way should ease the situation of the immigrants who are regularised. However, should high immigration flows continue, the problem will rear its head again. Those of us with a role to play must strive to mitigate it.